On May 29 this year, the National Commodity and Derivatives Exchange (NCDEX) listed India’s first SEBI-approved “weather derivative” named RAINMUMBAI. It is, in the most literal sense possible, a financial instrument whose entire value is: “how much did it rain in Mumbai?” But, trust me, it’s not as stupid as it sounds. The derivative has risen sharply by 30% since its launch as an intense monsoon lashes the city this month. This is as good an excuse as any to explain what it actually is, how we got here, and what the future looks like.

What is a Weather Derivative and Why are People Betting on the Rain?

Rain is bad for business. Sometimes in ways that are obvious: construction sites getting flooded, outdoor events getting cancelled, flights getting delayed. Sometimes in ways that aren’t: a hotel’s footfall dropping, a manufacturer’s raw material costs spiking due to poor harvests. Sometimes, an absence of rain is bad for business too if you run a hydroelectric power plant or are a farmer. The standard way to protect against losses from such natural events is to buy insurance. But insurance comes with a catch. You need to prove that you actually suffered a loss you’re claiming. And a long and tedious claim process could last longer than the monsoon itself, till which your business is underwater and you’re bankrupt. Many insurers don’t cover rain (or other weather risk) at all.

The alternative to buying insurance, then, is buying a (*drumroll*) weather derivative contract. This is a financial instrument or a “contract” (in the sense of being a legally binding agreement) designed to give you a payout when it rains more than a pre-agreed amount during a pre-agreed period (you get to choose both). If it pours, the payout covers your business losses from the rain, no questions asked. If it doesn’t, you don’t get a payout and lose the purchase price (just like insurance premiums), but it’s okay because your business is doing fine. These are generally listed and bought on exchanges – not stock exchanges, but those that sell derivative contracts like NCDEX.

Rain derivatives are an answer to a genuine gap and are a logical evolution in how Indians manage weather risk. When there was nothing else, farmers and entrepreneurs prepared for unfavourable rain through informal methods like savings, borrowing at high interest, and diversifying crops / operations geographically, which left them disastrously close to financial ruin. Then came government crop insurance schemes (CCIS and NAIS) which suffered from the same problems with insurance we discussed above and were riddled with bureaucracy, arbitrary disbursements, financial unviability, and called “a failure in all dimensions.”

Private ensurers soon devised a solution called “weather-indexed insurance” which is the closest we got to rain derivatives1. They paid out claims when the cumulative rainfall measured at weather stations over a period fell below/ above historical averages. These were a massive hit with farmers and India soon became the world’s largest weather-indexed insurance market, with the government launching its own version (WBCIS). Yet, these were still insurance contracts and had their limitations: you had to prove you had something to lose (insurable interest), you had to deal with an insurer, they weren’t tradable and only paid out at the end of the season, and required high premiums. Meanwhile, weather derivatives existed but were only available to large corporates who could ask a bank to make them a tailor-made instrument.

Rain derivatives freely available on an exchange are an improvement upon weather-index insurance products, while using the same basic idea that led to their widespread adoption. Hell, these derivatives could even end up making weather insurance cheaper as insurers hedge the risk of paying out claims by buying weather derivatives themselves.

Let me remind you that you don’t NEED to be a rain-impacted business or farmer to buy weather derivatives (though that was its original purpose). You could simply be someone with a demat account who thinks they’re good at predicting the weather.

How Does RAINMUMBAI Work?

So, here is how the derivative designed to save Mumbai from rain-induced financial ruin is designed:

- Availability. Listed on the NCDEX and available to trade between 10AM and 11:30PM. You can only buy contracts for periods between June and September (Mumbai monsoon months).

- What does it track? Tracks how far actual rainfall deviates from Mumbai’s 30-year average (2,206 mm). The 30-year period is called the long-period average (LPA) and the index recording the deviations is called the Cumulative Deviation Rainfall (CDR) index – just FYI. The actual rainfall will be measured by 2 automatic weather stations run by IMD at Santacruz and Colaba.

- Payout. Value goes up by ₹50 per mm of rainfall

- Last traded price (July 8, 2026). ₹2,882.10

It’s smart that the design builds around the rainfall index already in use in weather insurance. If it ain’t broke don’t fix it (or more appropriately, if it ain’t leakin’, stop tweakin’). Basing the derivative on just 2 weather stations at opposite ends of the city raises some questions as to whether it would accurately price how much it actually rained in the city. Heavy localised rainfall could impact businesses anywhere in the city-wide stretch from Colaba to Santacruz while rain barely falls on those 2 locations. Finance-bros call this “basis risk”. But starting small is natural and more stations may be expected in time2.

How is This Even Legal?

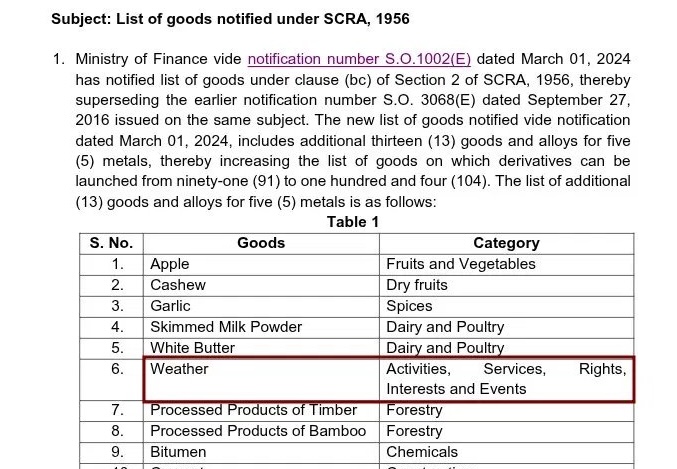

RAINMUMBAI is legally classified as a commodity derivative. Under the 1956 law (yes, 1956) that governs Indian financial instruments, a commodity derivative is a financial contract that “derives” its value from: (1) underlying goods (like gold, spices, silk… actual commodities), or (2) underlying activities, services, rights, interests and events as the government may decide.

If you really want something weird to be a commodity derivative, you would push for it to be included under the absurdly vague scope of (2). That’s what the government did with weather derivatives, making it 1 of the 2 items notified under (2) alongside freight through a SEBI circular on March 5, 2024. This paves the way for RAINMUMBAI and any future weather contracts to be legitimate derivatives and therefore “securities” in the legal sense and gives SEBI the right to oversee them.

Some (Hilarious) Thoughts

Mumbai doesn’t exactly have India’s largest farming population, but is a fertile testing ground for a product like this: a rainy, financially literate city, perpetually under-construction, headquartering all kinds of Indian business and a growing hub for global music festivals.

But I see the real fun beginning with RAINMUMBAI’s adoption as a speculation tool (rather than just loss-protection). Weather is hard but not impossible to predict. One could apply skill and technology to it, the way the IMD does but better (not a high bar). Hedge funds abroad like Millennium Management house teams of meteorologists and data scientists paid up to $1 million each to predict the weather and trade on it. If you’re a disillusioned meteorologist who doesn’t mind a bit of finance, now may be your time.

Second, market manipulation enforcement by SEBI will be a real treat to watch. And yes, weather-based instruments can be manipulated. In April this year, a trader in France used a hair dryer on a temperature gauge to change the recorded measurement after he bought a weather contract betting on rising temperature and is currently under investigation. Closer home in India, in the 2010-11 Rabi sowing season, there were reports of farmers placing ice cubes on the temperature sensors to trigger claims under weather-based insurance contracts. How long till someone takes a hose-pipe to an IMD automatic weather station? Should these stations have barbed wire? Stationed guards? CCTV cameras seem ideal.

Meanwhile, there is a chance that RAINMUMBAI becomes our most accurate predictor of rain in Mumbai once the market evolves. Financial markets serve as “truth machines”. When people with the best statistical models, satellite data, meteorological knowledge and overall understanding of rain stake their money on a certain probability of it raining, the price of RAINMUMBAI serves as an aggregation of all that knowledge and therefore the actual probability of rain. I hope, at some point of sophistication, I could look at RAINMUMBAI to plan my weekend more trustingly than the IMD forecast.

There are some expectations that NCDEX may expand beyond rainfall to other weather derivatives. The possibility is real, given SEBI’s 2024 green-light for all weather derivatives. Fun times ahead.

Footnotes

- The first weather insurance product in India (and in fact, the developing world) was launched in 2003 by ICICI-Lombard General Insurance Company for groundnut and castor farmers in Andhra Pradesh’s Mahabubnagar district as a pilot scheme. By 2007, over 539,000 farmers had purchased it. ↩︎

- When the US launched its first exchange-traded weather derivative, it was linked to just 10 cities in all of US. ↩︎